In the intricate dance of finance, credit risk assessment stands as a vigilant gatekeeper, ensuring that the delicate balance between opportunity and peril is meticulously maintained. As businesses and individuals alike seek to navigate the labyrinth of lending and borrowing, the ability to discern potential risks becomes paramount. Enter the realm of key metrics—those vital signposts that illuminate the path forward, guiding financial institutions with precision and foresight. In this article, we delve into the essential metrics that form the backbone of credit risk assessment, exploring how they empower decision-makers to craft strategies that are not only robust but also resilient in the face of uncertainty. With an authoritative lens, we unravel the complexities of these metrics, revealing their indispensable role in safeguarding financial stability and fostering sustainable growth.

Understanding Default Probability and Its Impact

In the intricate world of credit risk assessment, the concept of default probability stands as a cornerstone. This metric provides a quantifiable measure of the likelihood that a borrower will fail to meet their debt obligations. Understanding this probability is crucial, as it influences the decision-making process for lenders and investors alike. A higher default probability indicates a greater risk, which can lead to increased interest rates or the denial of credit altogether. Conversely, a lower probability often translates to more favorable terms for the borrower.

Key factors influencing default probability include:

- Credit History: A track record of timely payments can significantly lower default risk.

- Economic Conditions: Fluctuations in the economy can impact a borrower’s ability to repay.

- Debt-to-Income Ratio: A higher ratio may suggest financial overextension, raising default chances.

- Collateral Value: The presence of high-value collateral can mitigate perceived risk.

For financial institutions, accurately assessing default probability is not just about safeguarding their assets; it’s about strategically positioning themselves in the market. By leveraging sophisticated models and analytics, they can better predict and manage potential defaults, ensuring a robust and resilient credit portfolio.

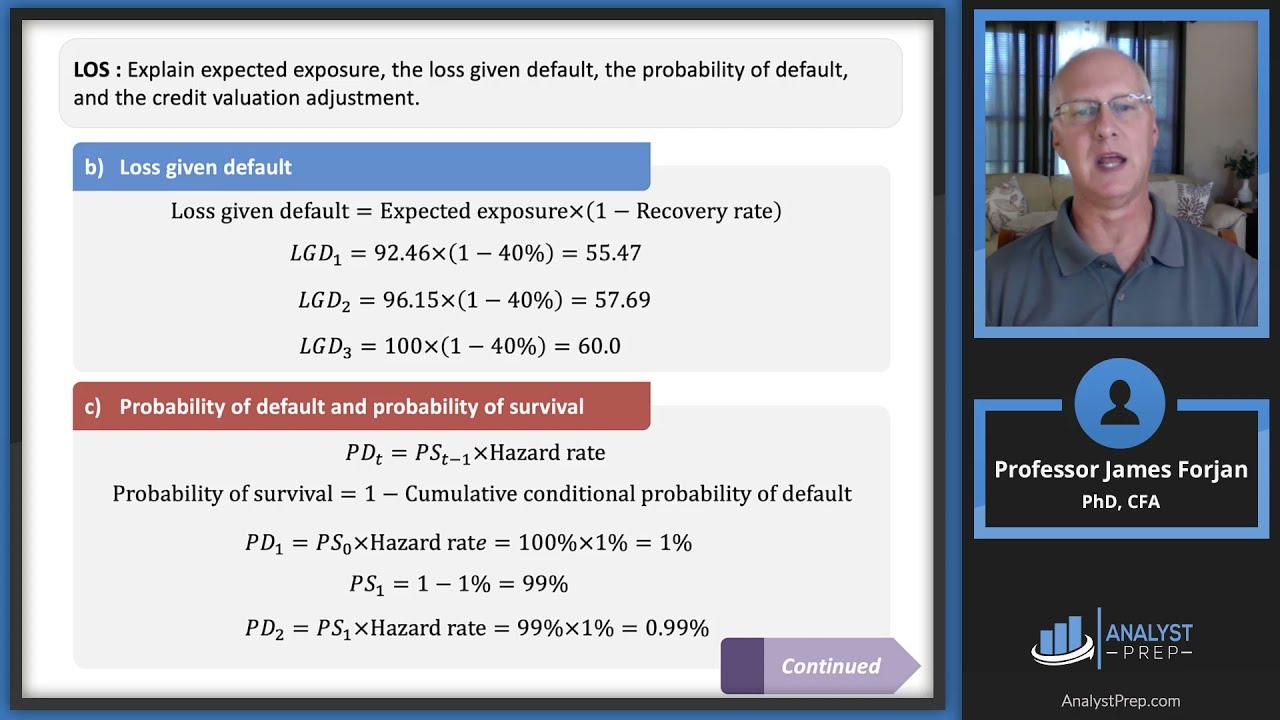

Decoding Loss Given Default for Better Risk Management

Understanding the intricacies of Loss Given Default (LGD) is pivotal for any financial institution aiming to bolster its risk management strategies. LGD, a critical component in the credit risk assessment process, quantifies the percentage of an asset’s value that is lost if a borrower defaults. By delving into LGD, institutions can better anticipate potential losses and adjust their risk mitigation tactics accordingly. To effectively decode LGD, it’s essential to consider various factors that influence it, such as:

- Collateral Quality: The type and value of collateral securing a loan can significantly impact the recovery rate post-default.

- Recovery Process Efficiency: The speed and effectiveness of the recovery process play a crucial role in minimizing losses.

- Market Conditions: Economic downturns or fluctuations can alter asset values, affecting the overall LGD.

By meticulously tracking these elements, financial institutions can refine their LGD models, leading to more robust credit risk management frameworks. This proactive approach not only enhances decision-making but also fortifies the institution against unforeseen financial adversities.

The Role of Exposure at Default in Credit Analysis

In the intricate tapestry of credit analysis, Exposure at Default (EAD) emerges as a pivotal metric, weaving together the threads of risk assessment and financial forecasting. EAD represents the total value a lender is exposed to when a borrower defaults on a loan. Understanding this metric is crucial for financial institutions aiming to gauge potential losses and tailor their risk management strategies effectively.

- Comprehensive Risk Assessment: EAD serves as a cornerstone for calculating potential credit losses, enabling analysts to predict the extent of financial exposure in worst-case scenarios.

- Strategic Decision-Making: By quantifying EAD, institutions can make informed decisions about capital allocation, ensuring resources are optimally distributed to mitigate risks.

- Enhanced Financial Modeling: Incorporating EAD into credit models enhances the accuracy of loss projections, providing a robust framework for stress testing and scenario analysis.

In essence, EAD not only illuminates the potential financial impact of defaults but also empowers lenders to fortify their defenses against credit risk, reinforcing the stability of their portfolios.

Leveraging Credit Scoring Models for Enhanced Accuracy

In the intricate world of credit risk assessment, harnessing the power of credit scoring models is crucial for achieving enhanced accuracy. These models, grounded in statistical algorithms, provide a robust framework for evaluating the creditworthiness of potential borrowers. To maximize their effectiveness, it is essential to focus on certain key metrics that can significantly influence the decision-making process.

- Probability of Default (PD): This metric estimates the likelihood that a borrower will fail to meet their debt obligations. By analyzing historical data and current financial behavior, credit scoring models can predict PD with remarkable precision.

- Loss Given Default (LGD): LGD assesses the potential loss a lender might incur if a borrower defaults. This metric is crucial for determining the severity of a default and aids in setting appropriate interest rates and credit limits.

- Exposure at Default (EAD): EAD measures the total value a lender is exposed to when a borrower defaults. Understanding this metric helps in calculating potential losses and in crafting risk mitigation strategies.

By closely monitoring these metrics, financial institutions can refine their credit scoring models, ensuring they not only predict defaults with greater accuracy but also optimize their risk management strategies. Such vigilance in tracking and analyzing these metrics empowers lenders to make informed decisions, safeguarding their portfolios while fostering responsible lending practices.

{kind=link}