In the intricate world of finance, where fortunes are built and lost on the tides of credit, understanding the nuances of credit risk assessment is akin to possessing a compass in a storm. At the heart of this discipline lies a set of powerful tools—key ratios—that serve as the financial analyst’s North Star, guiding them through the murky waters of creditworthiness evaluation. These ratios, though often cloaked in complexity, hold the secrets to deciphering the financial health and stability of borrowers, whether they be individuals, corporations, or entire nations. In this article, we will unravel the mysteries of these essential metrics, exploring how they illuminate the path to sound credit decisions and safeguard against the perilous pitfalls of financial uncertainty. Prepare to delve into the world of key ratios, where numbers tell stories and data drives destiny.

Understanding Liquidity Ratios for Predicting Financial Stability

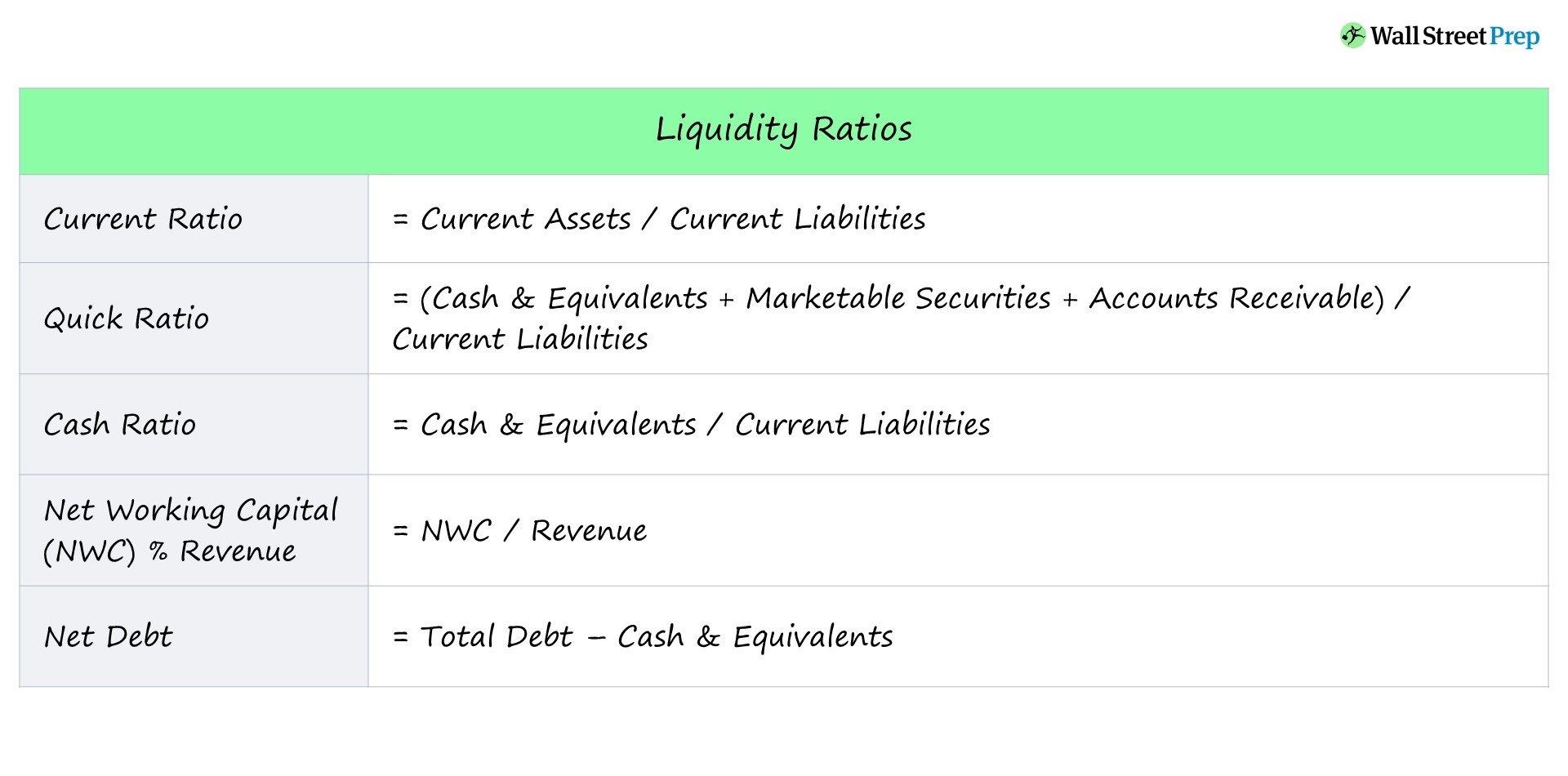

In the realm of credit risk assessment, liquidity ratios stand as crucial indicators of a company’s ability to meet its short-term obligations. These ratios provide insights into the financial health and operational efficiency of a business, serving as a beacon for investors and creditors alike. Current Ratio, Quick Ratio, and Cash Ratio are the triumvirate that analysts often rely on to gauge liquidity. Each of these ratios offers a different lens through which to view a company’s capacity to convert assets into cash quickly, without incurring significant losses.

- Current Ratio: This measures a company’s ability to cover its short-term liabilities with its short-term assets. A higher ratio suggests a more stable financial position.

- Quick Ratio: Also known as the acid-test ratio, this excludes inventory from current assets, providing a more stringent measure of liquidity.

- Cash Ratio: The most conservative of the three, it considers only cash and cash equivalents, offering a clear view of a company’s immediate liquidity.

By meticulously analyzing these ratios, stakeholders can anticipate potential liquidity challenges and make informed decisions. A robust understanding of these metrics not only aids in predicting financial stability but also enhances strategic planning and risk management efforts.

Analyzing Leverage Ratios to Gauge Long-term Solvency

Understanding a company’s leverage ratios is crucial for assessing its long-term solvency. These ratios provide insight into how a company finances its operations and whether it can meet its long-term obligations. Key leverage ratios include:

- Debt-to-Equity Ratio: This ratio compares a company’s total liabilities to its shareholder equity, indicating how much debt is used to finance assets relative to equity. A higher ratio may suggest greater financial risk.

- Interest Coverage Ratio: By measuring how easily a company can pay interest on its outstanding debt, this ratio helps assess financial health. A higher ratio indicates a stronger ability to meet interest obligations.

- Debt Ratio: This ratio shows the proportion of a company’s assets that are financed by debt. A lower ratio generally implies a more financially stable company.

Each of these ratios offers a unique perspective on a company’s financial structure, providing valuable insights for credit risk assessment. Analyzing these metrics helps investors and creditors determine the company’s ability to sustain operations and fulfill long-term commitments.

Evaluating Profitability Ratios for Insight into Earnings Potential

Understanding a company’s earnings potential is crucial when assessing its credit risk, and profitability ratios offer invaluable insights into this aspect. Gross Profit Margin is a fundamental metric, reflecting the efficiency with which a company produces goods or services. By analyzing this ratio, one can gauge how well a company manages its production costs relative to its sales. A higher margin indicates a robust ability to generate profit, which in turn suggests lower credit risk.

Another essential ratio is the Net Profit Margin, which provides a comprehensive view of a company’s overall profitability after all expenses have been deducted. This ratio is particularly insightful for assessing how well a company controls its operating costs and taxes. Additionally, the Return on Assets (ROA) ratio measures how effectively a company utilizes its assets to generate earnings. A high ROA indicates a strong earnings potential, making the company a more attractive candidate for credit. Monitoring these ratios helps credit analysts make informed decisions, ensuring a balanced approach to risk management.

Utilizing Coverage Ratios to Assess Debt Repayment Capacity

When evaluating a company’s ability to meet its debt obligations, coverage ratios serve as critical indicators. These ratios provide insight into how well a company can cover its interest payments and other fixed charges with its earnings. Among the most important coverage ratios are the Interest Coverage Ratio and the Debt Service Coverage Ratio (DSCR).

- Interest Coverage Ratio: This ratio is calculated by dividing a company’s earnings before interest and taxes (EBIT) by its interest expenses. A higher ratio suggests that the company is more capable of meeting its interest obligations, reflecting lower credit risk.

- Debt Service Coverage Ratio (DSCR): This measures the company’s ability to service its total debt, including both interest and principal payments. A DSCR greater than 1 indicates that the company generates sufficient income to cover its debt service, signaling financial stability.

By closely monitoring these ratios, investors and creditors can gauge the financial health of a company and its capacity to honor debt commitments, thus making informed decisions about credit risk.

{kind=link}