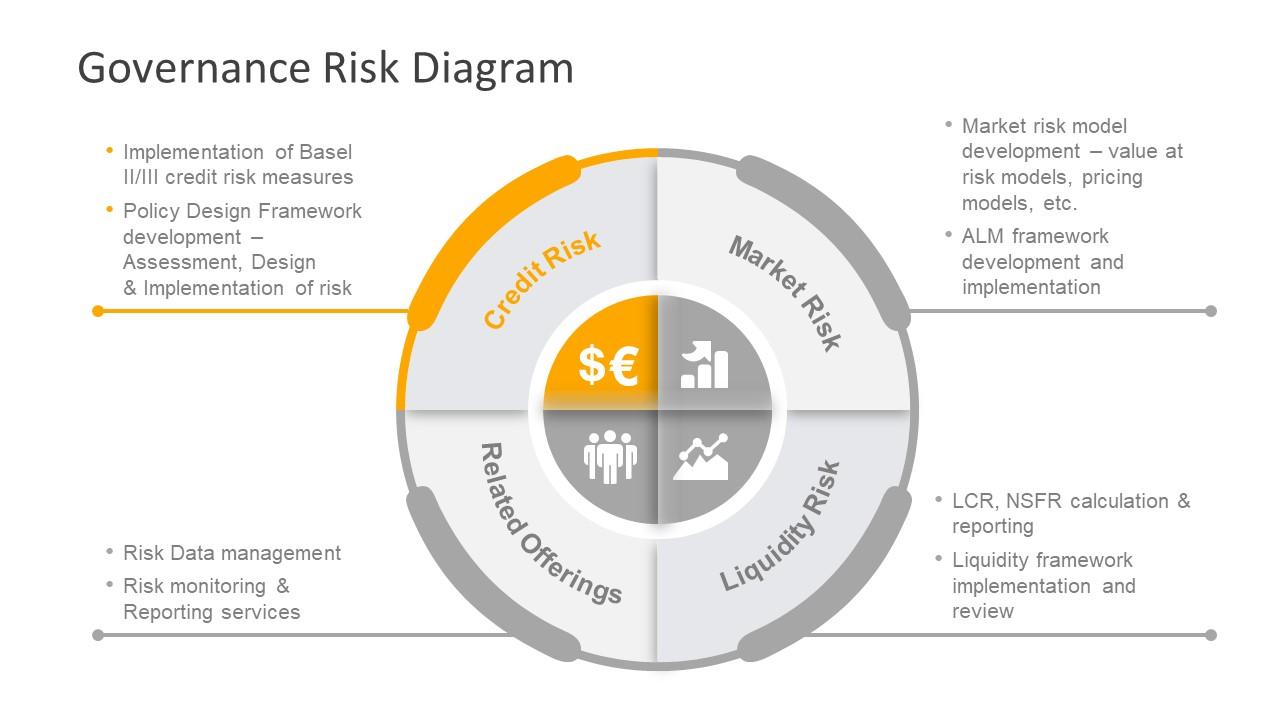

In the intricate dance of modern finance, credit risk is the shadow that follows every lender, a silent specter that can transform a promising opportunity into a perilous pitfall. As the global economy continues to weave an increasingly complex tapestry, understanding and mitigating credit risk has never been more crucial. Welcome to our exploration of the best practices for reducing credit risk, where we unravel the strategies that safeguard financial stability and illuminate the path to sustainable growth. With an authoritative lens, we delve into the art and science of credit risk management, equipping you with the insights needed to navigate this challenging landscape with confidence and precision. Whether you’re a seasoned financial professional or a curious newcomer, this guide will empower you to transform potential liabilities into opportunities for resilience and success.

Understanding the Landscape of Credit Risk Management

In today’s dynamic financial environment, effectively managing credit risk is crucial for maintaining a healthy balance sheet and ensuring long-term success. Financial institutions and businesses alike must employ robust strategies to mitigate potential losses arising from borrower defaults. Risk assessment and creditworthiness evaluation form the backbone of these strategies. It’s essential to leverage comprehensive data analytics to gain insights into borrowers’ financial health and predict potential risks. By utilizing predictive modeling and machine learning, organizations can identify early warning signs and take proactive measures.

Implementing a diversified credit portfolio is another critical best practice. By spreading credit exposure across various sectors, regions, and borrower types, businesses can reduce the impact of defaults in any single area. Additionally, maintaining stringent credit policies ensures that only borrowers meeting specific criteria are granted credit, thereby minimizing risk. Regularly reviewing and updating these policies to reflect changing market conditions is imperative. fostering strong relationships with borrowers through open communication can lead to better understanding and management of potential risks.

Crafting Robust Credit Assessment Frameworks

In the ever-evolving landscape of financial services, developing a resilient framework for credit assessment is crucial to mitigating potential risks. A robust framework should be dynamic, integrating both quantitative and qualitative data to ensure a comprehensive evaluation of creditworthiness. Financial institutions must focus on a multi-layered approach that incorporates the following best practices:

- Data Integration: Leverage a wide array of data sources, including traditional financial metrics and alternative data such as social media behavior and transaction patterns, to gain a holistic view of the borrower’s financial health.

- Advanced Analytics: Utilize machine learning and AI to enhance predictive accuracy. These technologies can identify patterns and anomalies that traditional models might overlook, offering deeper insights into credit risk.

- Continuous Monitoring: Implement real-time monitoring systems to track changes in a borrower’s financial situation. This proactive approach allows for timely interventions, reducing the likelihood of default.

- Regulatory Compliance: Ensure the framework aligns with the latest regulatory requirements, adapting swiftly to changes to maintain compliance and protect the institution’s reputation.

By integrating these strategies, financial institutions can build a credit assessment framework that not only safeguards against risk but also fosters sustainable growth and trust with their clientele.

Leveraging Data Analytics for Predictive Risk Modeling

In the rapidly evolving financial landscape, utilizing data analytics for predictive risk modeling has become an indispensable strategy for mitigating credit risk. By harnessing the power of advanced algorithms and machine learning, financial institutions can gain profound insights into customer behavior and potential risk factors. This proactive approach allows for the anticipation of default risks and the identification of early warning signals, enabling more informed decision-making.

- Data Integration: Combining data from diverse sources, such as transaction histories, social media, and market trends, creates a comprehensive view of a borrower’s financial health.

- Real-Time Monitoring: Implementing real-time analytics tools ensures continuous monitoring of credit portfolios, allowing for immediate action on emerging risks.

- Predictive Algorithms: Leveraging machine learning models that adapt over time enhances the accuracy of risk predictions, providing a dynamic and robust risk assessment framework.

By embedding these practices into their risk management processes, financial institutions can not only reduce the incidence of bad debt but also optimize their credit offerings, ultimately leading to a more resilient financial ecosystem.

Implementing Effective Risk Mitigation Strategies

In the ever-evolving landscape of credit risk, businesses must employ a multifaceted approach to safeguard their financial stability. Diversification is a cornerstone strategy, ensuring that credit exposure is spread across various sectors and geographical regions to minimize potential losses. This not only buffers against localized economic downturns but also leverages opportunities in emerging markets. Additionally, implementing robust credit scoring systems can significantly enhance risk assessment capabilities. By integrating advanced analytics and machine learning, companies can refine their predictive models, thus identifying potential defaulters with greater accuracy.

To further fortify against credit risk, businesses should establish a comprehensive credit policy framework. This involves setting clear guidelines on credit limits, payment terms, and conditions, tailored to the risk profile of each client. Regularly reviewing and updating these policies ensures they remain aligned with current market conditions and regulatory requirements. Moreover, fostering strong client relationships can provide invaluable insights into their financial health, enabling proactive measures to mitigate risks. Emphasizing transparency and open communication not only strengthens trust but also facilitates early intervention when signs of financial distress arise.

{kind=link}