In the intricate tapestry of modern finance, credit scoring models stand as the silent arbiters of opportunity, wielding the power to unlock doors to homes, cars, and dreams. Yet, for many, these enigmatic algorithms remain shrouded in mystery, their decisions as cryptic as the ancient oracles. This article aims to demystify the arcane world of credit scoring, peeling back the layers to reveal the mechanics and logic that govern these digital gatekeepers. With an authoritative lens, we will journey through the labyrinth of data points and mathematical models, illuminating how they collectively shape the financial destinies of millions. Prepare to embark on a voyage of understanding, where numbers transform into narratives, and the abstract becomes accessible.

Understanding the Mechanics Behind Credit Scores

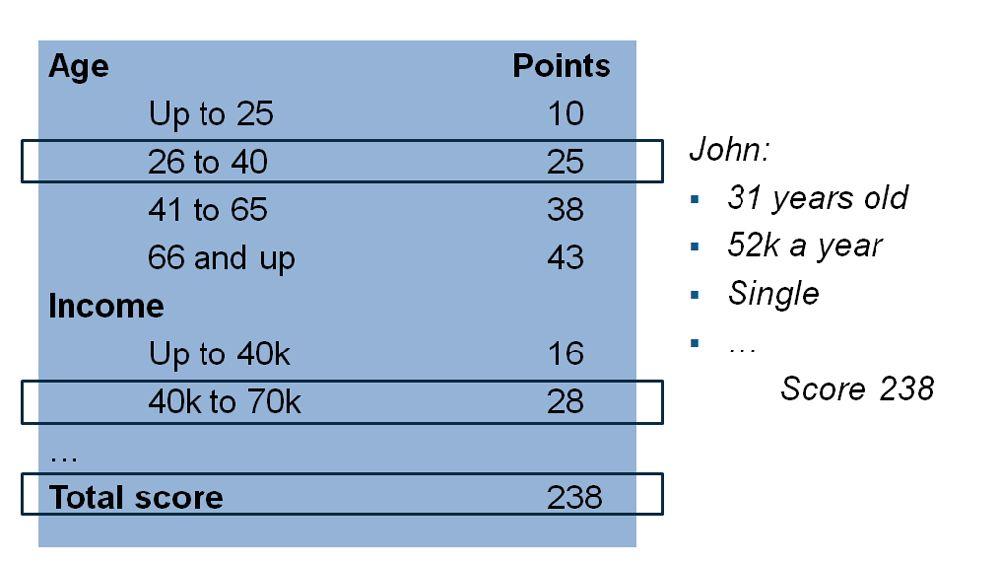

At the heart of credit scoring models lies a complex algorithm that evaluates an individual’s creditworthiness based on a variety of factors. These models, often shrouded in mystery, operate on a blend of data points to produce a three-digit score that can significantly impact one’s financial opportunities. To demystify this process, it’s essential to understand the core components that most credit scoring models consider:

- Payment History: This is the most significant factor, reflecting whether you’ve paid past credit accounts on time. Late payments, defaults, and bankruptcies can severely affect your score.

- Credit Utilization: This ratio compares your current credit card balances to your credit limits. A lower ratio indicates responsible credit management, positively influencing your score.

- Length of Credit History: A longer credit history provides more data points for assessing risk, often leading to a higher score if managed well.

- Types of Credit: A diverse mix of credit accounts, such as credit cards, mortgages, and auto loans, can enhance your score by demonstrating your ability to manage different types of credit.

- New Credit Inquiries: Frequent applications for new credit can signal financial distress and may lower your score temporarily.

Understanding these elements is crucial, as each plays a unique role in the credit scoring tapestry. By focusing on these areas, individuals can take proactive steps to improve their credit scores, unlocking better financial opportunities and terms.

The Role of Data in Shaping Your Credit Profile

Data is the backbone of your credit profile, intricately woven into the fabric of credit scoring models. Every financial move you make—whether it’s paying off a loan or missing a credit card payment—contributes to a complex tapestry of information. This data is meticulously analyzed to determine your creditworthiness. The algorithms used in credit scoring models sift through vast amounts of information to paint a picture of your financial habits. They consider a variety of factors, such as:

- Payment History: Timely payments boost your score, while late payments can significantly harm it.

- Credit Utilization: The ratio of your credit card balances to your credit limits is a critical component.

- Length of Credit History: A longer credit history often indicates reliability.

- Types of Credit: A diverse mix of credit accounts can positively impact your score.

- Recent Credit Inquiries: Multiple inquiries in a short period can be a red flag.

By understanding how data shapes your credit profile, you can take proactive steps to manage your financial reputation effectively. Harnessing the power of data not only empowers you to make informed decisions but also enhances your ability to navigate the financial landscape with confidence.

Demystifying the Algorithms: A Deep Dive into Credit Scoring Formulas

In the intricate world of credit scoring, algorithms serve as the silent architects of financial trustworthiness. These complex formulas, often shrouded in mystery, are designed to assess the risk associated with lending money to individuals. Credit scoring models analyze a multitude of factors, transforming raw data into a numerical score that predicts the likelihood of a borrower defaulting on a loan. At the heart of these models are key components that include:

- Payment History: A record of your past financial behavior, this element accounts for a significant portion of your score, emphasizing the importance of consistent, on-time payments.

- Credit Utilization: The ratio of your current credit balances to your credit limits. Maintaining a low utilization rate can positively impact your score.

- Length of Credit History: The duration of your credit activity. A longer history can demonstrate reliability and experience in managing credit.

- Types of Credit: A diverse mix of credit accounts, such as credit cards, mortgages, and auto loans, can indicate a well-rounded financial profile.

- New Credit Inquiries: Recent applications for credit can signal financial distress, potentially lowering your score.

Each of these elements is meticulously weighed and balanced, forming the backbone of the scoring process. While the exact algorithms remain proprietary secrets, understanding these components provides valuable insight into how your financial actions influence your credit score.

Strategies to Optimize Your Credit Score for Financial Success

Understanding the intricacies of credit scoring models is pivotal in crafting strategies that bolster your financial health. At the core, these models evaluate a myriad of factors to calculate your creditworthiness. Payment history stands as a critical element, reflecting your reliability in meeting financial obligations. A consistent record of timely payments can significantly enhance your score. Another key factor is your credit utilization ratio, which is the proportion of your credit card balances to your credit limits. Keeping this ratio below 30% is generally recommended to maintain a favorable score.

Beyond these, several other components influence your credit score. Consider the length of your credit history; a longer track record often suggests stability. Additionally, a diverse mix of credit accounts—such as credit cards, mortgages, and installment loans—can positively impact your score, demonstrating your ability to manage various types of credit. be mindful of new credit inquiries; while it’s natural to seek new credit occasionally, frequent applications can be perceived as risky behavior. By focusing on these elements, you can strategically navigate the credit landscape and optimize your score for financial success.

{kind=link}