In the intricate dance of modern finance, where every step can mean the difference between prosperity and peril, understanding the subtle language of numbers is paramount. At the heart of this numerical symphony lies a powerful tool: financial ratios. These ratios, often seen as the DNA of a company’s financial health, offer a window into the complex world of credit risk management. As businesses navigate the turbulent waters of global markets, the ability to interpret and leverage these ratios becomes not just a skill, but an art form. This article delves into the strategic use of financial ratios, unraveling their secrets to empower decision-makers in safeguarding their enterprises against the looming specter of credit risk. With precision and insight, we explore how these mathematical indicators can illuminate the path to financial stability and resilience, transforming potential vulnerabilities into opportunities for growth and security.

Understanding Financial Ratios: The Key to Effective Credit Risk Management

In the intricate world of finance, the ability to decode numbers is akin to possessing a compass in a dense forest. Financial ratios serve as this compass, guiding businesses through the complex landscape of credit risk management. These ratios are more than mere numbers; they are the lifeblood of strategic decision-making. By analyzing these figures, businesses can gain a deeper understanding of their financial health and creditworthiness. Key ratios such as the Current Ratio, Debt-to-Equity Ratio, and Interest Coverage Ratio provide invaluable insights into a company’s liquidity, leverage, and ability to meet its financial obligations.

- Current Ratio: A measure of a company’s ability to cover its short-term liabilities with its short-term assets.

- Debt-to-Equity Ratio: This ratio reveals the proportion of a company’s financing that comes from creditors and investors, offering a glimpse into its financial leverage.

- Interest Coverage Ratio: It indicates how easily a company can pay interest on its outstanding debt, highlighting its financial stability.

Mastering these ratios allows businesses to anticipate potential financial pitfalls and make informed decisions. It empowers them to negotiate better terms with lenders, optimize their capital structure, and ultimately safeguard their financial future. In a world where uncertainty is the only certainty, understanding and leveraging financial ratios is not just a skill—it’s a necessity.

Leveraging Liquidity Ratios for Informed Credit Decisions

Understanding and utilizing liquidity ratios can significantly enhance the decision-making process when it comes to assessing credit risk. These ratios, which include the current ratio, quick ratio, and cash ratio, offer a snapshot of a company’s ability to cover its short-term obligations with its most liquid assets. By analyzing these metrics, credit managers can gain insights into the financial health and operational efficiency of a potential borrower. For instance, a high current ratio might indicate a robust liquidity position, suggesting that the company is well-prepared to meet its short-term liabilities. Conversely, a low quick ratio could signal potential liquidity issues, warranting a more cautious approach.

Incorporating liquidity ratios into credit risk management involves more than just number crunching. It’s about understanding the story behind the numbers. Consider the following strategies:

- Trend Analysis: Examine the historical trends of liquidity ratios to identify patterns or anomalies that might indicate emerging risks.

- Industry Benchmarks: Compare the liquidity ratios against industry averages to gauge the company’s standing relative to its peers.

- Comprehensive Evaluation: Use liquidity ratios in conjunction with other financial metrics for a holistic view of the company’s financial health.

By effectively leveraging these ratios, credit professionals can make more informed decisions, ultimately leading to a more resilient credit portfolio.

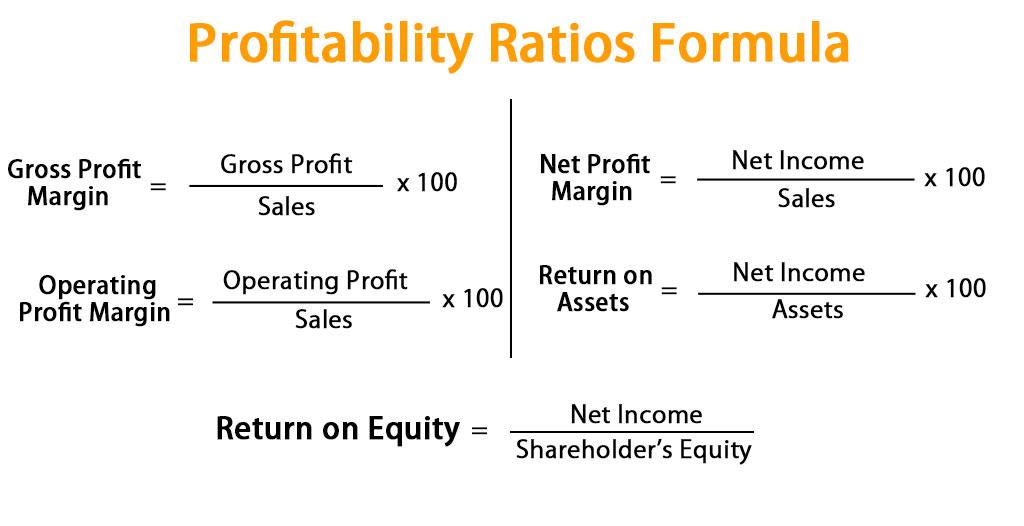

Harnessing Profitability Ratios to Gauge Borrower Stability

In the realm of credit risk management, profitability ratios serve as a vital compass, guiding lenders through the intricate landscape of borrower evaluation. These ratios, which include the net profit margin, return on assets (ROA), and return on equity (ROE), provide a snapshot of a borrower’s financial health and operational efficiency. By analyzing these metrics, lenders can discern the ability of a borrower to generate profit relative to their revenue, assets, and equity. This insight is crucial in assessing whether a borrower can sustain operations and meet financial obligations, thus ensuring stability and minimizing risk.

- Net Profit Margin: Reveals how much profit a company makes for every dollar of revenue, indicating cost control and pricing strategy effectiveness.

- Return on Assets (ROA): Measures how efficiently a company uses its assets to generate profit, offering a glimpse into operational efficiency.

- Return on Equity (ROE): Assesses the return generated on shareholders’ equity, highlighting the company’s ability to reward its investors.

For lenders, a thorough understanding of these ratios can be transformative, enabling them to make informed decisions that balance opportunity with caution. By integrating profitability ratios into their credit risk management framework, financial institutions can enhance their ability to identify robust borrowers and mitigate potential losses.

Strategic Use of Solvency Ratios to Mitigate Credit Exposure

In the intricate landscape of financial management, solvency ratios emerge as a powerful tool to strategically manage credit exposure. These ratios, which include the debt-to-equity ratio, interest coverage ratio, and equity ratio, provide a comprehensive view of a company’s financial health and its ability to meet long-term obligations. By leveraging these metrics, businesses can assess their capacity to sustain operations during economic downturns, thereby minimizing the risk of default.

- Debt-to-Equity Ratio: This ratio highlights the proportion of debt and equity used to finance a company’s assets, offering insights into financial leverage and stability.

- Interest Coverage Ratio: By examining the company’s ability to pay interest on outstanding debt, this ratio serves as a critical indicator of financial endurance.

- Equity Ratio: This metric reflects the proportion of a company’s assets financed by shareholders’ equity, underscoring the strength of the capital structure.

By maintaining optimal levels in these ratios, companies can not only enhance their creditworthiness but also negotiate better terms with lenders. The strategic use of solvency ratios enables businesses to make informed decisions, ensuring a robust financial foundation that mitigates credit exposure effectively.

{kind=link}