In the ever-shifting landscape of global finance, the specter of inflation looms large, casting its shadow across markets and economies with a transformative force. As nations grapple with rising prices and fluctuating currencies, the world of credit risk finds itself at a pivotal crossroads. Once a relatively stable domain governed by well-worn metrics and established models, credit risk is now undergoing a metamorphosis, adapting to the relentless march of global inflation. This evolution is not merely a reactionary shift but a profound recalibration, as financial institutions and analysts alike strive to navigate the turbulent waters of economic uncertainty. In this exploration, we delve into the intricate ways in which credit risk is being reshaped, uncovering the innovative strategies and tools emerging in response to inflationary pressures. Join us as we unravel the complexities of this new era, where the rules are being rewritten and the stakes have never been higher.

Navigating the New Landscape of Credit Risk Amidst Global Inflation

In the face of surging global inflation, credit risk management is undergoing a significant transformation. Financial institutions are now compelled to adopt more dynamic and proactive strategies to mitigate the evolving risks. Traditional models, which heavily relied on historical data, are proving inadequate in the current volatile economic climate. Instead, there’s a shift towards real-time data analysis and predictive analytics, enabling lenders to anticipate potential defaults more accurately and adjust their risk assessments accordingly.

- Enhanced Monitoring: Banks are increasingly investing in technology to enhance their monitoring capabilities, allowing for quicker responses to economic changes.

- Diversification of Portfolios: By diversifying their credit portfolios, institutions can spread risk across different sectors and geographies, reducing exposure to inflation-sensitive industries.

- Collaboration with Fintech: Collaborations with fintech companies are on the rise, providing banks with innovative tools and platforms to better assess and manage credit risk.

These strategic shifts underscore the necessity for agility and foresight in credit risk management, as institutions strive to safeguard their assets while navigating the complexities of a high-inflation environment.

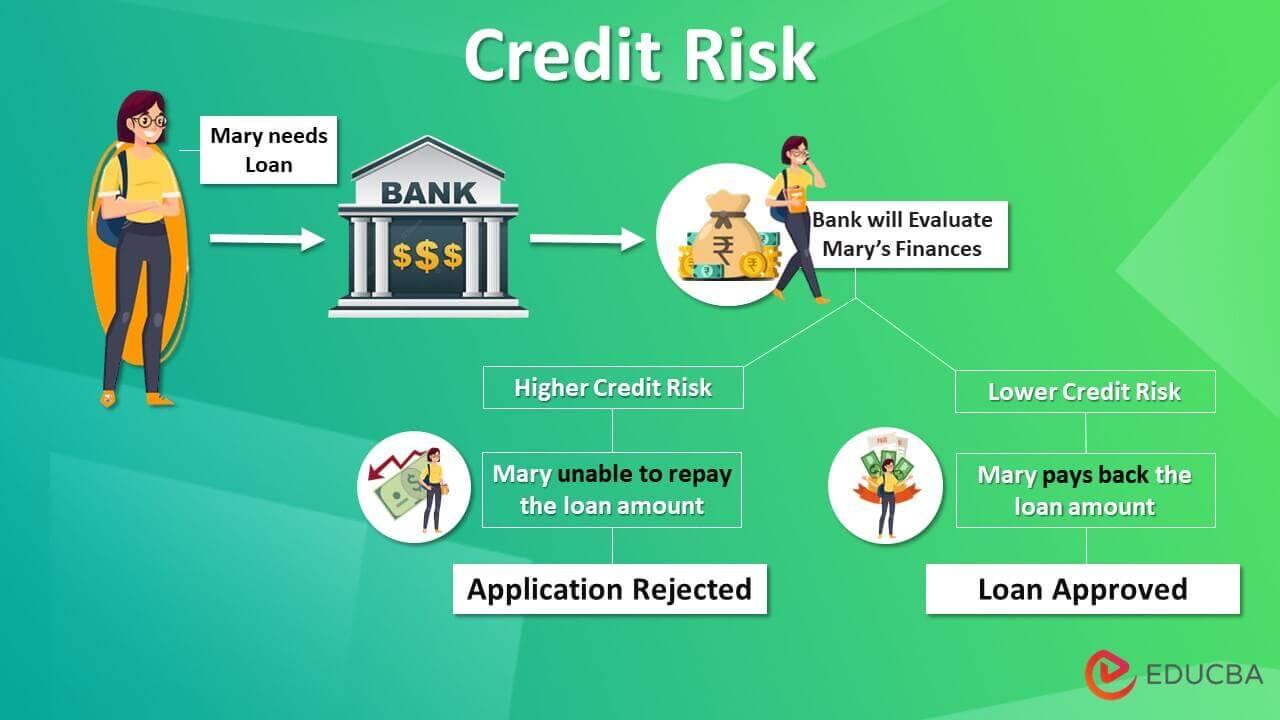

Understanding the Impact of Inflationary Pressures on Creditworthiness

As global inflation continues to rise, the financial landscape is experiencing a seismic shift, directly affecting the creditworthiness of individuals and businesses alike. Inflationary pressures often lead to increased interest rates, which in turn, elevate the cost of borrowing. This scenario can strain the financial health of borrowers, making it challenging for them to meet their debt obligations. Consequently, lenders are compelled to reassess their risk models, incorporating new variables to better gauge the potential for default.

- Income Volatility: With inflation eroding purchasing power, borrowers may experience fluctuations in disposable income, impacting their ability to service debt.

- Asset Valuation: Inflation can distort asset prices, complicating the assessment of collateral value and affecting loan-to-value ratios.

- Debt Servicing Costs: As interest rates climb, so do the costs associated with servicing existing debt, potentially leading to higher default rates.

These factors necessitate a more dynamic approach to credit risk assessment, where lenders must not only rely on historical data but also anticipate future economic conditions. This evolution in credit risk management underscores the need for financial institutions to adopt advanced analytical tools and strategies, ensuring they remain resilient in the face of ongoing inflationary challenges.

Strategic Approaches to Mitigating Inflation-Induced Credit Risks

In the face of rising global inflation, financial institutions are adopting innovative strategies to shield themselves from the heightened credit risks. A key approach is the diversification of loan portfolios, which involves spreading credit exposure across various sectors and geographies. This strategy reduces the impact of localized economic downturns and inflationary pressures on specific industries. Financial institutions are also leveraging advanced data analytics to enhance their risk assessment models. By integrating real-time economic indicators and consumer behavior data, these models provide a more nuanced understanding of borrower risk profiles in an inflationary environment.

Additionally, many organizations are revisiting their credit underwriting standards. By tightening lending criteria and incorporating inflation forecasts into credit evaluations, lenders can better anticipate potential defaults. Some institutions are also turning to hedging strategies to manage interest rate risks associated with inflation. These include the use of financial derivatives to lock in borrowing costs and protect against rate fluctuations. Together, these strategic approaches form a robust framework for navigating the complexities of inflation-induced credit risks, ensuring financial stability and resilience in uncertain times.

Innovative Risk Assessment Tools for a Volatile Economic Environment

In today’s rapidly changing economic landscape, traditional methods of evaluating credit risk are being supplemented by innovative tools designed to navigate the complexities of global inflation. These cutting-edge solutions are leveraging advancements in technology and data analytics to provide a more nuanced understanding of potential financial threats. By integrating artificial intelligence and machine learning, financial institutions can now analyze vast datasets in real-time, allowing for more accurate predictions and proactive risk management.

- AI-Powered Analytics: Machine learning algorithms can identify patterns and trends that were previously undetectable, offering insights into potential risk factors.

- Blockchain Technology: Enhances transparency and traceability, reducing fraud and increasing trust in financial transactions.

- Predictive Modeling: Advanced models can simulate various economic scenarios, helping institutions prepare for potential market shifts.

- Sentiment Analysis: By analyzing social media and news feeds, these tools can gauge public sentiment and its potential impact on financial markets.

As these tools continue to evolve, they are reshaping the landscape of credit risk assessment, enabling businesses to remain resilient amidst economic volatility. The integration of these technologies not only enhances accuracy but also ensures that financial institutions are better equipped to adapt to the ever-changing global economy.

{kind=link}